A real estate market forecast shows buying depends on your location, timeline, and finances—not broad market timing.

The question “Is it time to buy a home?” feels urgent. And it should—housing is usually the biggest financial decision most people make. But the honest answer depends entirely on your situation, not on whether the market is “good” or “bad” right now.

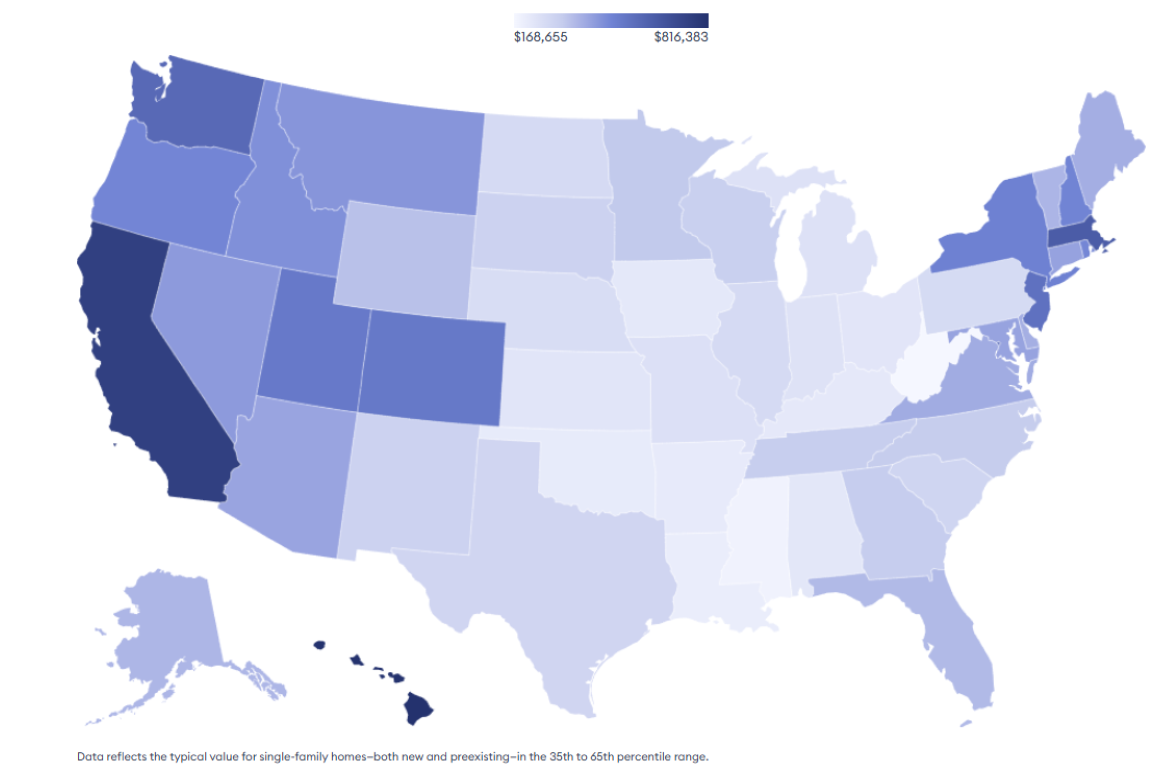

Here’s what the real estate market forecast for 2026 actually tells us: the market is fragmented. National trends are nearly useless. What matters is where you live, what you can afford, and whether buying aligns with your life plan. Let me break down what’s actually happening and what it means for your decision.

Regional Markets Are Pulling in Different Directions

The biggest shift in recent years is that real estate is hyper-local. One national “market” doesn’t exist anymore.

Northeast and Midwest markets are seeing higher demand and steadier price growth. These regions offer what buyers increasingly want: more space, lower list prices, and proximity to jobs. Secondary cities—places that aren’t major metros—are gaining serious traction. If you’re in these regions, inventory is tighter and buyer competition is real, but the fundamentals are sound.

West Coast markets (California especially) are cooling. Slower growth, more inventory coming to market, and longer days on market give buyers more leverage here. If you’ve been waiting to buy in California, conditions are shifting in your favor—but prices are still steep.

The Sunbelt (Florida, Texas, Arizona) is stabilizing after years of pandemic-era appreciation. Prices shot up fast. Now they’re flattening. This can actually be a decent entry point if you’re willing to wait a few months and negotiate.

Smaller metros in low-supply regions consistently outperform when buyers balance affordability and access to jobs.

Interest Rates Will Likely Stay Higher Than You’d Like

Mortgage rates are expected to average around 6.3% in 2026, down from recent highs but nowhere near the 3% we saw in 2020-2021. This matters because it directly impacts what you can afford.

A 0.5% drop in rates pulls buyers off the sidelines. We’ll likely see that happen. But it won’t feel dramatic. Your monthly payment on a $400,000 home at 6.3% versus 6.8% saves you roughly $75/month—meaningful but not transformative.

The real impact: higher rates favor buyers who can move fast and negotiate. Properties priced right sell in days. Overpriced homes sit for 60+ days. If you’re ready to buy and you find a well-priced property, your position is strong. Sellers know rates aren’t dropping fast, and they’re more flexible than they were two years ago.

Inventory Is Rising—Slowly, and Not Everywhere

Limited housing inventory is the core issue across most markets, but it’s starting to loosen. More homes are coming on the market, especially in specific regions. This gives you more choices and better negotiating power than you had in 2023-2024.

However, inventory isn’t the same everywhere. In hot Northeast and Midwest markets, supply is still tight. In cooled Sunbelt markets and California, you’ve got more options. Know your local market. Pull data on months of supply in your area—if it’s under 4 months, it’s a seller’s market; above 6 months, it’s a buyer’s market.

Price Growth Is Slowing (But Prices Aren’t Dropping)

Expect modest appreciation in 2026—typically 4-6% year-over-year in stable markets. That’s healthy growth without the 10-15% spikes we saw during the pandemic.

This is important: you’re not “late” if you buy now, nor will you “miss out” if you wait 6 months. At 4-6% annual appreciation, you’re building equity steadily. On a $500,000 home, that’s $20,000-$30,000 in appreciation annually—solid, but not life-changing month-to-month.

What actually matters more than catching the perfect bottom: eliminating rent increases, locking in your housing payment, and building equity in an asset you control.

The Real Buying Decision Isn’t About Market Timing

Here’s the reality most people miss: the “best time to buy” isn’t when the market is cheapest. It’s when these conditions align:

- You have 10-20% down (or enough to avoid PMI if that matters to you)

- You can afford the payment plus taxes, insurance, and 1% of the purchase price annually for maintenance

- You plan to stay in the home 5+ years (to absorb buying/selling costs)

- You’re buying in a region with actual job growth and population demand

- Your life situation is stable (job locked in, family plans clear, not planning to relocate)

If those five things are true, the market conditions in 2026 are reasonable. Not perfect, but reasonable. Waiting for a “better” market often means paying higher rents for another 2-3 years and watching prices appreciate anyway.

If any of those are false? Waiting makes sense. Build savings. Lock down your job. Get your life situation clearer. Then revisit.

The Bottom Line

Is it time to buy a home? It depends on you, not on the real estate market forecast. The 2026 market offers a healthier, more balanced environment than 2023-2024—more inventory, slower price growth, slightly more buyer leverage. Rates are still elevated, but stable.

Your decision should rest on your finances, your timeline, and your region. Stop waiting for “the perfect moment.” Focus on being in the position to act when the right property in the right neighborhood becomes available at the right price—for you.

Want a clearer framework for making big financial decisions like this? Explore Making The Most for practical guidance on housing decisions, financial planning, and life systems that actually work.